What tax code should be used for new starters and leavers? Can I use a P45 tax code from a previous tax year? How should payments on leaving employment be taxed?

This is a freeview 'At a glance' guide to which PAYE code to use for starters or leavers.

At a glance

Starters

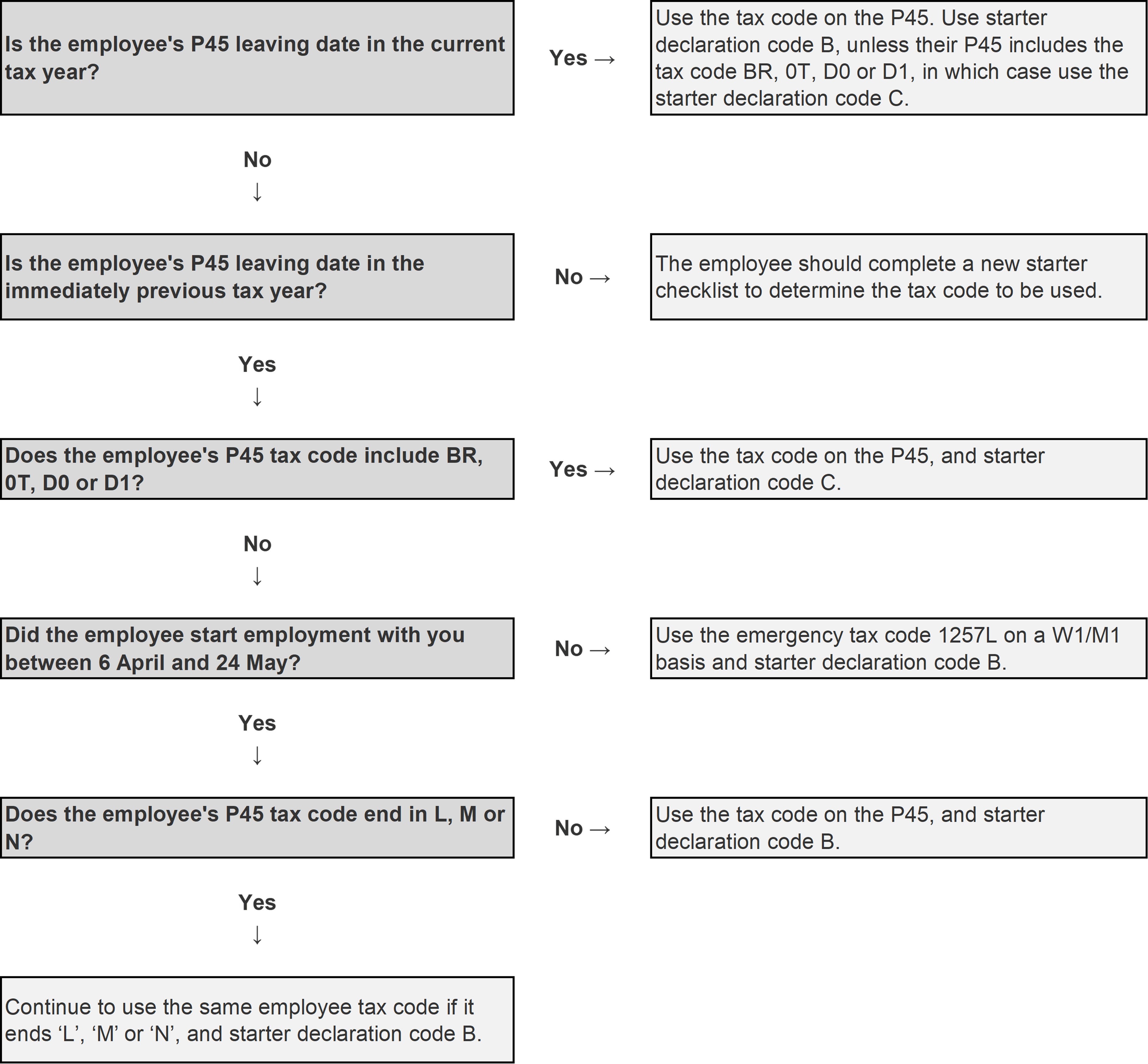

Starters with a P45: refer to Starters: P45 flowchart tab.

Starters with no P45:

- If completed a starter checklist, apply the code produced.

- If unable to complete a starter checklist, apply code 0T on a week 1/month 1 basis and starter declaration code C.

Leavers

- Cash-based payments: use code 0T on a week 1/month 1 basis.

- Share-based payments: use 0T on a week 1/month 1 basis, see below.

- Pensionable leavers: use the employee’s existing tax code on a week 1/month 1 basis until a new code is received from HMRC. A cumulative basis code can be used if the first pension payment is in the new tax year.

Leavers in more detail

Employers should use the 0T code for all leavers, except:

- Leavers to whom the employer will pay a pension (above).

- When a P45 has not yet been issued.

- Certain share-based payments.

- When an NT code is in operation.

When a form P45 has not yet been issued

When no P45 has been issued:

- Employers should issue a P45 on the last date of employment.

- It may be impossible to issue a P45 on that day, so there may be a gap between leaving and the final payroll run. If so, use the last Pay-As-You-Earn (PAYE) code for the final payroll run and then issue the P45.

If Form P45 has been issued:

- Regulation 37 PAYE Regulations 2003 applies: use code 0T on a week 1/month 1 basis.

Share-based payments

- Use an 0T code on a week 1/month 1 basis once a P45 has been issued unless the employee was on an NT code, see below.

- When there are a series of payments see HMRC guidance: Share-based payments.

Leavers with an NT code

- An NT code is given for non-resident employees. If an NT code is in operation do not change this to an 0T code for a leaver.

Starters: P45 flowchart

Use this flowchart to determine the tax code to use for a new employee for tax year 2025-26 and 2026-27 where they provide form P45.

Note: W1/M1 = week 1/month 1 basis.

Small print & links

Useful guides on this topic

What is the 2025-26 PAYE tax code?

What is the 2025-26 PAYE tax code? What do the different types of tax code prefixes and suffixes mean?

What is the 2026-27 PAYE tax code?

What is the 2026-27 PAYE tax code? What do the different types of tax code prefixes and suffixes mean?

PAYE: Starter checklist new employee 2025-26

Freeview PAYE starter checklist. Use this form if you are taking on a new employee.

PAYE: Starter checklist new employee 2026-27

Freeview PAYE starter checklist. Use this form if you are taking on a new employee.

RTI: Real-Time Information for PAYE

What is RTI: Real-Time Information (RTI) reporting for PAYE? How does it work?

Legislation

Income Tax (Pay as You Earn) Regulations 2003 SI 2003/2682