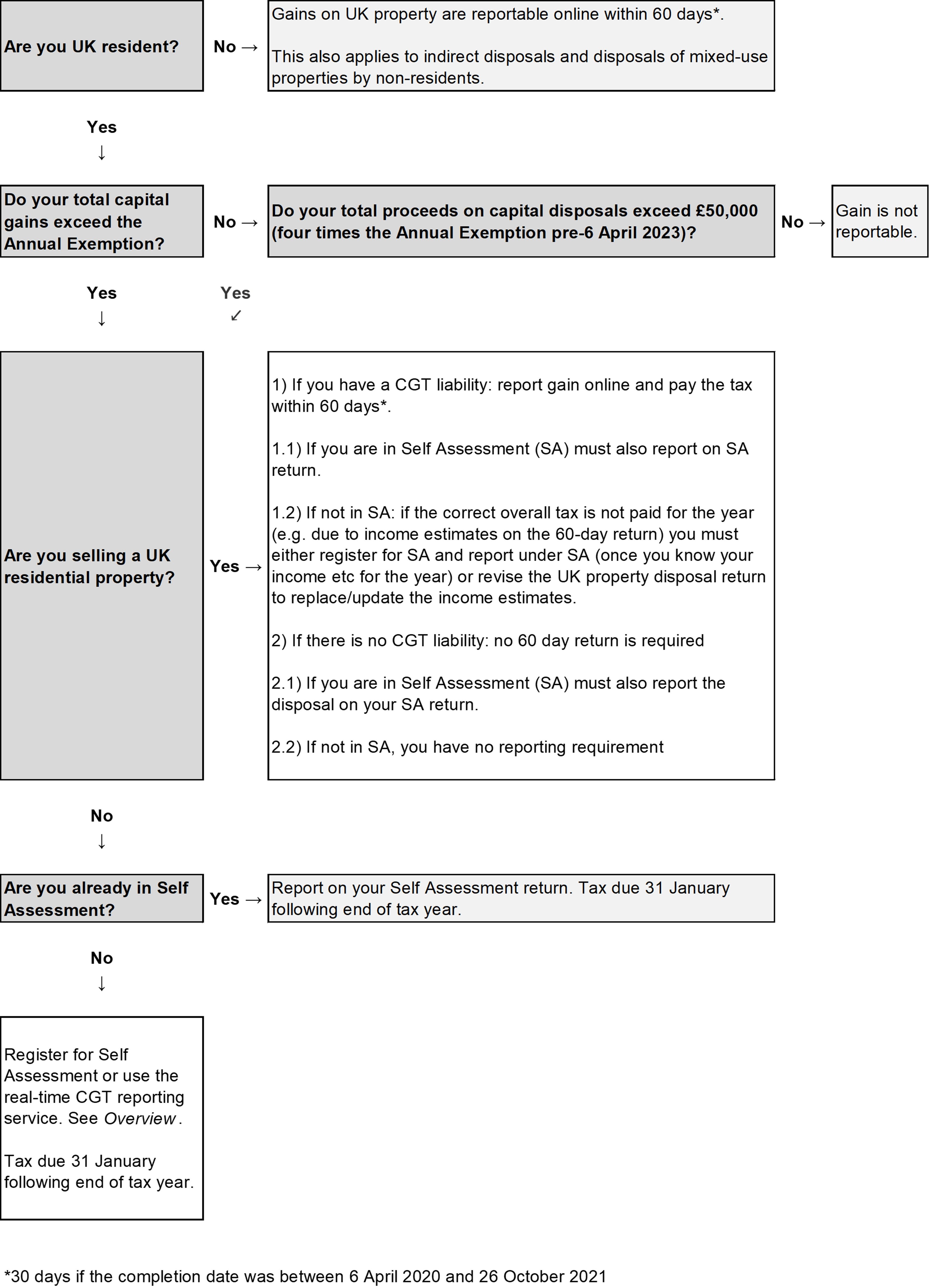

How do you report your capital gains? What return do you use? There are different ways for individuals to report capital gains depending on whether you are resident or non-resident, and whether you are in or out of Self Assessment.

This is a freeview 'At a glance' guide about how to report capital gains.

At a glance

For individuals only: disposals on or after 6 April 2020

Overview

UK resident

Reporting requirement for disposals on or after 6 April 2020 (UK residents)

Capital gains may be reported via the:

- Self Assessment tax return.

- Real-time CGT reporting service.

Disposals of UK residential property can also fall within the separate UK property reporting service. This is discussed further below.

Where an individual is within Self Assessment, their tax return must include all capital disposals where:

- The total gains exceed the available Annual Exemption.

- The total proceeds are more than £50,000 for 2023-24 onwards or four times the Annual Exemption for earlier years (for 2020-21 to 2022-23 this was £49,200),

The exception to this is where the whole gain is covered by Private Residence Relief.

If total gains are below the Annual Exemption and total proceeds do not exceed £50,000 (or four times the Annual Exemption where relevant), they do not need to be reported to HMRC.

If an individual is not registered for Self Assessment, they do not need to report gains if there is no tax payable.

If CGT is payable and the disposal does not relate to UK residential property, the taxpayer can report the gain by either:

- Registering for Self Assessment.

- Using the Real-time CGT reporting service (see below).

UK residential property (from 6 April 2020)

Gains on UK residential property disposals must be declared on HMRC's online UK property disposal return, and the tax paid, using the Capital Gains Tax UK property reporting service, within:

- 60 days if the completion date was on or after 27 October 2021.

- 30 days if the completion date was between 6 April 2020 and 26 October 2021.

If no CGT is due the online return does not need to be filed. In determining whether any tax is due, only losses incurred by the date of completion may be taken into account.

The UK property disposal return must be completed even if the gain has already been reported under Self Assessment (SA), except where the gain is declared under SA first because the SA return is filed before the 60-day deadline. In this case, no online UK property disposal return is required. See 60-day CGT returns required despite reporting under Self Assessment

Planning point: if the Self Assessment Tax return can be submitted within 60 days of completion no separate CGT return is required. This also defers the tax liability until 31 January following the end of the tax year. This situation can occur when the property exchange and completion fall in different tax years.

- Example: exchange occurs on 1 March 2024 (2023-24) and completion occurs on 15 May 2024. The UK property disposal return must be completed by 14 July 2024, unless the 2023-24 tax return showing the disposal is submitted before 14 July 2024. If the 2023-24 tax return is submitted by 14 July 2024, this moves the CGT due date to 31 January 2025.

Self Assessment (SA) reporting continues in parallel to the 60-day rule (previously 30 days).

Further reporting obligations:

- Any adjustments to the figures or reliefs claimed can be made under SA and the tax due will be adjusted accordingly.

- If you are not already in SA, you can register and include the gain on your SA return but you are not required to if you do not have any other reportable income or gains.

- From 14 October 2020, it is possible to amend HMRC's online UK property disposal return after the 60-day window within the normal SA amendment window.

- Amendments are only to be permitted "so far as the return could, when originally delivered, have included the amendment by reference to things already done". It would seem that any changes that do not meet this condition will need to be addressed in the SA return instead.

- Typical reasons for amendment can include:

- The estimate of the individual's income changes, resulting in the rate of CGT needing amendment.

- The value of estimated or apportioned amounts becomes known.

- It becomes reasonable to conclude that a relief under TCGA 1992 will apply.

- A provision of TCGA 1992 will apply because of the individual's residence status.

- HMRC announced that they would not charge penalties for late returns by UK residents until after 31 July 2020. See Changes to CGT reporting: Soft landing period for penalties

Practical points:

- For mixed-use properties, where there is an identifiable residential part e.g. a flat over business premises, a UK property disposal return is required if the residential property disposal gives rise to a gain with CGT due. Only the residential part of the gain is required to be reported in the UK property disposal return. If there will be no CGT to pay on the residential element of the gain, then there is no need for a UK property disposal return to be filed.

- If the disposal of the non-residential part results in a loss, this loss could be offset against the residential element when working out if you must file a UK property disposal return.

- The grant of an option over residential property resulting in a capital gain triggers a requirement to file a return and pay the CGT within 60 days, despite the fact that the grant and exercise of an option are generally treated as a single transaction on the later date that the option is exercised.

Paper returns:

- Since 6 April 2024, HMRC has provided an alternative 'interactive form' that taxpayers or their agents can complete online, to print and post, where the online service cannot be used.

- This form covers all tax years between 2020 and 2025.

- It is necessary to report by post in cases such as where the taxpayer:

- Has already submitted an SA return for the same tax year as the report.

- Needs to amend a paper form which has already been sent to HMRC.

- Cannot use the online service.

- For those who cannot manage the interactive form, it will be necessary to call HMRC to request a paper return.

- From 28 February 2023, the form could also be downloaded from HMRC, as a PDF, but this facility was replaced by the interactive form (above) on 6 April 2024.

- Due to the length of time that paper returns take, HMRC have said that the 60-day clock for payment of CGT will be paused once the paper return is received to allow them time to process the return and to contact the taxpayer with details of how to make payment.

- HMRC have advised that where a paper return has been used and it is necessary to wait for HMRC to issue a demand to pay, taxpayers will have 60 days (previously 30 days) from the issue date to settle the tax.

Administration:

- Taxpayers who do not have a UK passport or credit history may have difficulty completing the Government Gateway verification process: if this is the case, they are advised to complete the interactive form (or if it is not possible, the paper form).

- When making payments, taxpayers must ensure that they quote either their CGT account reference number or payment reference number to enable their payment to be allocated to their account.

- Payments made should be available to view on the dashboard in three to five days once the payment has cleared.

- The online property return enquiry window for taxpayers not in Self Assessment is generally one year from 31 January following the end of the tax year of disposal. The enquiry window for disposals in the 2022-23 year ends on 31 January 2025.

- The 30/60-day return enquiry window for taxpayers who are in Self Assessment is generally 12 months from the submission of the Self Assessment tax return.

Using an agent to report disposals on or after 6 April 2020:

- Agents can report disposals on behalf of clients but must be specifically authorised to do so via their Agent Services Account (ASA) as existing 64-8 forms do not cover this.

- The client must first set up a Capital Gains Tax on a UK property account. They will be issued with a 15-digit reference number.

- The client then passes their reference number and postcode to their agent who can request authorisation to manage the client's CGT property account. They do this through their ASA.

- The client will receive a link to click on to approve the agent to act. Once approved, the agent can prepare and file the return for the client.

- Once the return is filed the agent and client should receive an email from HMRC with instructions for making payment. It appears that payment cannot be made simultaneously with the filing of the return as a reference is required.

- Anyone who cannot authorise their agent online and does not wish to file an interactive/paper return can go through a telephone authorisation process with HMRC instead.

- Once an agent is authorised this will continue until the client removes it and a new agent cannot be authorised until the old one is removed. If they wish another agent to act without replacing their existing agent the new agent will have to file an interactive form instead.

- The exception to this is for estates. Agents can only submit interactive forms on behalf of Personal Representatives (PRs) as there is not yet any facility for PRs to authorise agents online. However, the PRs can file online returns themselves by setting up an online property account.

Trustees who need to report disposals:

- Where a trust needs to report a gain on a residential property sale and has not already registered under the Trust Registration Service (TRS), it will need to do so before it can report the gain and pay the Capital Gains Tax. This also applies to non-resident trusts. See Trust Registration Service.

- Corporate trustees must file paper returns.

Real-time CGT reporting: outside Self Assessment

- If you are outside the Self Assessment regime, you do not have to register for Self Assessment just to report a capital gain.

- Instead, for pre-April 2020 disposals of residential property, and for all other gains (pre and post-April 2020), you can use HMRC’s ‘real-time’ service.

- You can report your capital gain anytime between the date you have prepared your capital gain calculations and 31 December following the end of the tax year in which the capital gain took place.

- For example, if you sold a holiday home at a gain in June 2023, you can report the gain using the real-time service up to 31 December 2024. You could also have reported it before the end of the 2023-24 tax year if you wished.

- You will need to have or set up a Government Gateway account.

- PDF or JPG copies of your calculations will need to be attached to your submissions.

- The deadline for the tax remains 31 January following the end of the tax year, though HMRC will issue a payment reference number once they have processed the gain so that you can make payment sooner if you wish.

- The main benefit of this system is that it allows for immediate calculation, reporting, and if necessary, payment of capital gains, which will ensure penalties and interest are avoided.

- If you prefer you can register for Self Assessment and report the gain on a Tax Return.

Real-time CGT reporting: already in Self Assessment

- If you are already in Self Assessment, you can still use the real-time service.

- If you choose to report under the real-time service, you will still have to report the gain on your tax return as well.

Reporting requirement for disposals before 6 April 2020

- If you make a capital gain you will need to report it to HMRC if:

- The total of your gains exceeds your available Annual Exemption.

- The total proceeds are more than four times the Annual Exemption.

- If the total gains are below the Annual Exemption and total proceeds do not exceed four times the Annual Exemption, you are not required to report them to HMRC.

- If you have a reportable capital gain(s) before 6 April 2020 you can report this to HMRC in two ways:

- Using HMRC’s ‘real time’ Capital Gains Tax (CGT) service.

- Completing the Self Assessment tax return.

Non-UK residents

- Non-UK residents are partly outside of the UK CGT regime.

- From April 2015, UK residential property sold at a capital gain is subject to Non-Resident CGT (NRCGT).

- From April 2019, all non-resident UK property sales and Indirect disposals of an interest in a 'UK property-rich' entity are subject to NRCGT whether the property is residential or commercial.

- See Non-Resident Capital Gains Tax (NRCGT).

- All disposals must now be reported within 60 days of completion of conveyance (30 days before 27 October 2021)

For NRCGT disposals on or after 6 April 2020

- All NRCGT must be paid within:

- 60 days if the completion date was on or after 27 October 2021.

- 30 days if the completion date was between 6 April 2020 and 26 October 2021.

- This applies whether the non-resident is in Self Assessment or not. See CGT: Payment of tax.

- HMRC's 'Capital Gains Tax UK property disposal service' must be used by the non-resident or their agent/adviser to report the disposal, except in the following circumstances where the NRCGT return can continue to be used:

- Disposals of mixed-use properties, e.g. part residential, part commercial such as a doctor's surgery or shop with a flat above.

- Indirect disposals of a property-rich entity where at least 75% of the gross asset value is attributable to UK property.

- The disposal must be declared even if there is no tax due and/or there is a loss.

- The non-resident taxpayer can set up a UK property account within the new service here without needing a government gateway ID, by going to 'Create sign-in details' and providing an email address.

- An agent can report the disposal on the non-resident's behalf but they must first set up a UK property account as they will need to provide the agent with the account number as well as their country of residence.

For NRCGT disposals before 6 April 2020

- The NRCGT must be paid within 30 days unless the non-resident is already in Self Assessment, in which case it can be paid by the normal 31 January deadline. See CGT: Payment of tax

Repayment of CGT

As CGT is payable within 60 days of a disposal, it may not be possible at that time for a taxpayer to know what their total Income Tax liability will be for the year.

In order to offset CGT paid against Income Tax, the taxpayer or their agent should phone HMRC on 0300 200 3300 or the agent dedicated line, to ask HMRC to manually offset the CGT paid against their Income Tax liability.

Alternatively, if there is time, you should amend the UK property disposal return and this will allow a refund via the CGT system. If this is done before submitting the SA return this will avoid the need for HMRC to create a manual override.

CGT Property Disposal Return FAQ

When must UK property disposal returns be filed?

UK property disposal returns must be filed within 60 days of the completion date of the property disposal.

For disposals prior to 26 October 2021, they must have been filed within 30 days of completion.

What is the interaction between UK property disposal returns and Self Assessment returns?

UK property disposal returns must be filed before filing the Self Assessment return. Disposals cannot be reported on a UK property disposal return after a Self Assessment return has been filed.

The only exception to this rule is where the Self Assessment tax return is filed within 60 days of the completion of the property transaction. This situation removes the requirement to file a UK property disposal return.

HMRC have confirmed that where a property return should have been filed but the gain has subsequently been reported through Self Assessment, an interactive form/paper property return should still be filed. The interactive form can be downloaded here. If the taxpayer is unable to obtain the interactive form, a paper property return can be requested from HMRC by phone.

We understand that HMRC will not impose daily late filing penalties of £10 for late property returns.

When can I make payments of tax due?

CGT payments due as a result of a UK property disposal return cannot be made until the return has been processed.

When HMRC process the return, they will issue a payment reference which needs to accompany the payment.

Can I appoint an agent to deal with my UK property disposal return?

An agent can be appointed using Form 64-8. However, as there is no way to limit this authorisation to deal with only UK property disposal returns, completing a 64-8 would remove the authority for an existing agent.

A ‘digital handshake’ procedure is also available whereby an individual gives their CGT on UK Property Account number and UK postcode (or country of residence if non-UK resident) to an agent. The agent then submits those details on their agent account which results in the individual receiving an authorisation email they then need to pass back to the agent.

See HMRC guidance at CG-APP18-120

Do I need to file online?

An interactive/paper return is needed in certain situations. This includes where a taxpayer is prevented from setting up a government gateway account due to being unable to meet the identity options available and non-residents who are not otherwise required to obtain a Unique Tax Reference number.

HMRC guidance provides an alternative sign-in process for non-residents who do not have a UTR or National Insurance number: See: CG-APP18-160

To file online, Trusts (both UK and non-UK) must be registered under the Trust Registration Service (TRS) prior to being able to file the CGT return online. A paper return can be requested (or downloaded) by trustees where there is no CGT liability and no requirement to obtain a trust UTR or register via TRS.

What if I make multiple property disposals on the same day, do I need to file a separate return for each of them?

- If you sell more than one property on the same day (same completion date) you can declare them all on one single return.

- The return through the CGT on UK Property Account only records a single address, so you should include the details of the property which results in the largest gain when prompted for property details. You will then be required to upload further details explaining the CGT calculated for all the properties you are reporting which will allow you to add in the address for the other properties.

What if I am digitally excluded?

- HMRC has introduced a new process to allow agents to report and pay using the Capital Gains Tax (CGT) UK property disposal online service on behalf of clients who are digitally excluded.

The process is:

- Agent registers with Agent Services unless they have an existing account.

- Agent asks their client to contact HMRC to register for a CGT on UK Property Account.

- HMRC adviser will confirm the client is digitally excluded and refer them to a Tax Technician.

- The Tax Technician follows the registration process resulting in the client receiving a CGT on UK Property Account reference.

- The client gives the CGT on UK Property Account reference to their agent to begin the agent-client authorisation process.

- Agent logs into Agent Services and selects ‘Ask your client to authorise you’.

- Agent enters their client’s CGT Account reference, creating an invitation link.

- The client contacts HMRC to request support to authorise their agent and provides their CGT on UK Property Account reference.

- HMRC advisor refers to the Extra Support Team and the client receives a call back within 48 hours.

- HMRC Extra Support Service adviser calls the client and confirms they are happy for the agent to act on their behalf and creates the agent-client relationship.

- The agent can engage digitally with HMRC on behalf of their client for CGT property disposals.

How can I claim a repayment or tax offset?

Disposals can need reporting on both a UK property disposal return and through Self Assessment.

For the 2020-21 tax year, where a UK property disposal return liability was higher than that in the Self Assessment tax return, it was necessary to phone HMRC to request a manual offset of that excess payment.

This should not be the case for 2021-22 and subsequent years, any excess payment should automatically be offset against any Self Assessment liability. If the Self Assessment is in a refund position, HMRC should be contacted to request a repayment of CGT paid under the UK property disposal return.

If no Self Assessment return is filed, the CGT position can be finalised by submitting an amended property return.

How do I claim Business Asset Disposal Relief (BADR) on the UK property disposal return?

- If you are selling a residential property eligible for BADR e.g. a furnished holiday let, you can claim the relief on the UK property disposal return by selecting 'Yes' to the question 'Does the person want to claim any other CGT reliefs?'

- For disposals in which BADR is claimed the CGT must be worked out manually. The CGT figure produced by the inbuilt calculator should be overridden with the figure worked out manually and a computation showing how the CGT amount due has been calculated will need to be attached.

Small print & links

Useful guides on this topic

SRT: Statutory Residence Test ToolkitThis is a freeview interactive tool to determine 'At a glance' whether you are UK resident or not in a tax year. A tax year in the UK runs 6 April to 5 April.

Non-resident CGT: UK propertyHow and when does Capital Gains Tax apply to non-residents owning UK property?

External links

Capital Gains on UK property account